We’ve all been there. You’re short a little bit to get groceries this week. Sounds like a deal to buy whatever you want now and make 4 easy payments that are interest free.

Hold up. Let's stop right there! Those payments may be interest free, but that doesn’t mean it’s the way go. Let’s look a few key factors:

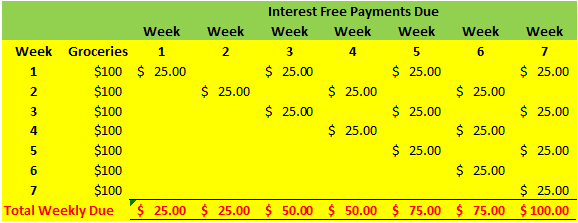

Making Ends Meet

Let’s say you need $100 of groceries every week. Look at the chart and see what happens if you buy $100 of groceries every week on buy now pay later. By week 7 you are making $100 in payments on payment plans from groceries from 4 other weeks before you even buy your $100 of groceries for week 7. Do you have $200 in your budget for week 7? Or, will you have to buy now and pay later again, paying $125 in week 7 and building on future weeks. This sounds more like digging a hole than getting out of one.

Hold up. Let's stop right there! Those payments may be interest free, but that doesn’t mean it’s the way go. Let’s look a few key factors:

Making Ends Meet

Let’s say you need $100 of groceries every week. Look at the chart and see what happens if you buy $100 of groceries every week on buy now pay later. By week 7 you are making $100 in payments on payment plans from groceries from 4 other weeks before you even buy your $100 of groceries for week 7. Do you have $200 in your budget for week 7? Or, will you have to buy now and pay later again, paying $125 in week 7 and building on future weeks. This sounds more like digging a hole than getting out of one.

Now consider if you’re short again or you have too many payment plans in place and miss a payment during week 7. While there is no interest, you are charged a late fee. Klarna, for example, charges a $7 late fee for each missed payment, so if in week 7 you have 4 payments due from prior weeks and miss them, you’ve now spent $28 more, still owe Klarna $100 and don’t have the $100 you need for this week’s groceries. And the hole gets deeper.

Effects on Credit Score

Beyond the finances, banks that offer buy now pay later may run credit checks. If they are soft credit checks, they will not impact your credit score. Hard credit checks will show up on your credit score and cause it to go down. Banks like Klarna may run credit checks, but they don’t usually report your payment information to the credit bureaus, so while a late payment won’t impact your credit, your timely payments are not building good credit either. If you miss too many payments, your account could be referred a collection agency. These collection agencies do report the delinquency to credit bureaus and your credit score will go down.

Spending More Than You Can Afford

The danger is that buying now and paying later encourages you to spend more than you can afford. Even though these banks convince you that you are "saving money" by not paying interest, it’s super easy to go over your budget and get into debt or stall your progress toward your other financial goals.

The Takeaway

Unless your kids are hungry and you can’t buy them food, think twice about using buy now pay later. Even if your kids are hungry, opt for help from family/friends, the food bank or other programs that serve meals to people who cannot afford food.

If what you want to buy is not an essential for survival like food, such as a cool pair of shoes or sporting equipment that you cannot afford to pay for now, it’s best to go old school. Save now and buy later.

Say you have a budget of $25/mo. for clothing and want to buy a pair of shoes that costs $100. It’s better to save for 4 months until you have enough to buy the shoes. If you go into debt for them there will be other things that will be wanted or needed when the payments come due, and the debt will grow.

First, before buying consider a few things:

• Do you really need those cool new shoes? Or would they be just for keeping up with the Jones’ and looking cool? If you have a pair of shoes that are in working condition, maybe you don’t really need another pair. You can only wear one pair at a time. Essentials come first.

• Is the sporting equipment essential? Could you buy used sporting equipment that would do the same job for less money? Check Craigslist. Share with a friend. And, if you do decide to buy new, always shop for the best prices.

Would you like to create a working budget to pay down your debt, save for a home, or just make ends meet? Give us a call and we can help you reach your goals!

Effects on Credit Score

Beyond the finances, banks that offer buy now pay later may run credit checks. If they are soft credit checks, they will not impact your credit score. Hard credit checks will show up on your credit score and cause it to go down. Banks like Klarna may run credit checks, but they don’t usually report your payment information to the credit bureaus, so while a late payment won’t impact your credit, your timely payments are not building good credit either. If you miss too many payments, your account could be referred a collection agency. These collection agencies do report the delinquency to credit bureaus and your credit score will go down.

Spending More Than You Can Afford

The danger is that buying now and paying later encourages you to spend more than you can afford. Even though these banks convince you that you are "saving money" by not paying interest, it’s super easy to go over your budget and get into debt or stall your progress toward your other financial goals.

The Takeaway

Unless your kids are hungry and you can’t buy them food, think twice about using buy now pay later. Even if your kids are hungry, opt for help from family/friends, the food bank or other programs that serve meals to people who cannot afford food.

If what you want to buy is not an essential for survival like food, such as a cool pair of shoes or sporting equipment that you cannot afford to pay for now, it’s best to go old school. Save now and buy later.

Say you have a budget of $25/mo. for clothing and want to buy a pair of shoes that costs $100. It’s better to save for 4 months until you have enough to buy the shoes. If you go into debt for them there will be other things that will be wanted or needed when the payments come due, and the debt will grow.

First, before buying consider a few things:

• Do you really need those cool new shoes? Or would they be just for keeping up with the Jones’ and looking cool? If you have a pair of shoes that are in working condition, maybe you don’t really need another pair. You can only wear one pair at a time. Essentials come first.

• Is the sporting equipment essential? Could you buy used sporting equipment that would do the same job for less money? Check Craigslist. Share with a friend. And, if you do decide to buy new, always shop for the best prices.

Would you like to create a working budget to pay down your debt, save for a home, or just make ends meet? Give us a call and we can help you reach your goals!